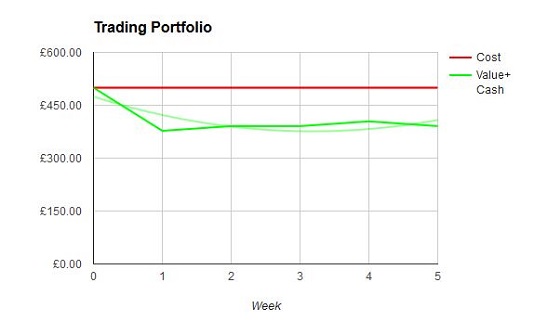

I figured the portfolio review should be in order of the percentage of my portfolio the company makes up, so without further ado here we go.

I should stress that everything below is my opinion and may or may not even be factually correct, as I don't particularly know what I'm talking about. It's meant as notes to myself to remind me why I invested in something and a reminder of what I want to top up or get rid of. There is no intention for any of this to be considered advice, so in the time-honoured words of all the stocks and shares websites, "do your own research".

AMYT:Amryt Pharma 9.5%

Currently down 20% and losing £849.19

I first spotted this share when is was

FAST:Fastnet Oil & Gas when I read it had sold up the oil and gas side of the business. It then became Fastnet Equity and started to search for a pharma company to buy out.

I bought more shares at this point, because I felt a company with the sense to get out of oil just before the crash had a good chance of finding something worth buying.

I'm hoping I was right, as when they announced the reverse takeover of Amryt Pharma I bought some more, and more, and then more.

The key for me is the involvement of Harry Stratford as Chairman. He took

SHP:Shire Pharma from a startup to a massive company with a share price of 5,145p. He's applying exactly the same formula to Amryt, seeking out orphan diseases with no existing treatment and developing treatments that will dominate the market, as well as improving people's lives.

My repeat purchases have taken my average price from the initial 24p at the time of the reverse takeover to 17.5p. I now have 28,454 shares, so if I'm right and this takes off, it could be remarkable.

For this one I'm definitely buying the management team - trusting their strong track record will come good despite the dreadful looking chart. I will aim to up my holding to 10% of my portfolio while the price is so low.

OPTI:Optibiotix 9.5%

Currently down 10% and losing £598.67

This is my favourite share. You wouldn't believe it from the performance, but this is the one I believe can make me huge amounts of money. That's why I kept buying at 86p when I should have waited for the drop to 78p. Never mind, those 8p will be nothing once this takes off.

I've bought a promise. A promise of a cure for obesity, of a new type of sugar that acts like a fibre and can be eaten safely by diabetics, of a skin treatment that can combat MRSA.

I've also bought the promise of the company being split into four separate companies, with me being allocated shares in all of them.

Apart from the daily ups and downs, this share has been flat for a year. It appears to be a major institutional investor that was very heavily invested in the early days selling for a 100%+ profit so they can fund other startups. They appear to be controlling the selling of their shares to prevent the share price tanking and to ensure they keep making their profit. The effect seems to be that whenever the share looks like it will break out, it sinks back slightly and is bound between 75p and 80p. It's just my misfortune to have bought on a spike.

I don't know when this selling will stop, but when it does, and with a few news releases, this share could go bonkers.

The first commercial product using the "Slimbiome" bacteria in the "Go Figure" range has hit retail stores in a joint venture, and early reviews have been very favourable, so this could be the kick start the shares need.

I thought this was my biggest investment at 10%, but writing this has shown it's the same as

AMYT:Amryt Pharma at 9.5%. In that case, I feel a top up is on the cards while still below 80p!

CAML:Central Asia Metals 6.4%

Currently up by 2% and making £62.47

My favourite company (as opposed to share) - it's so well managed and so generous to shareholders.

For some reason the share price keeps tanking, but I have no clue why, as they were making good profits even when the price of copper was at rock bottom. They can produce it so cheaply, they will just keep churning out the cash and the massive 7.6% dividend.

I will definitely keep adding more to this one. If I was allowed to invest my monthly amount in AIM companies, I'd invest it in this, but that's restricted to FTSE 250 and 100.

I will aim to get to 10% of my holding in this one over time.

They have paid back more in dividends to shareholders than they got for their listing, and have a gigantic pile of cash waiting to pounce on a new low-cost project when it comes available. Most likely one is Copper Bay in Chile, which is being investigated now.

This is such a well run company that I have massive confidence in it's long-term value for my SIPP

CWR:Ceres Power Holdings 4.7%

Currently up 26% and making £741.68

I bought this on the story. A steel and enamel power cell that can generate electricity efficiently when heat is applied. Existing partnerships with boiler manufacturers and car manufacturers ooze potential. The possibility of fitting a Ceres power pack into a domestic boiler to generate electricity. The possibility of putting multiple power packs together into small regional power stations. No more turbines, just gas powered electricity direct from the power pack. The possibility of putting into a hydrogen powered electric car, with far better distance and re-fueling time than a lithium-ion battery.

It's a risky share as they have nothing generating revenue yet. The plan is to licence the production of the power cell to partner companies rather than manufacture it themselves, although they do have a small production line churning out a fuel cell every 3 seconds.

I think 4.7% of the portfolio is probably enough for this one, as I'm not as confident as I am with the 10% shares. If a commercial deal is announced and there's still time to buy cheap, then I may get a few more.

GVC:GVC Holdings 4.4%

Currently up 64% and making £1,490.31

Probably my best overall share. I've already sold a third of the holding for a £236 (27.5%) profit, but glad I kept the other two thirds, as they have absolutely soared.

I bought them because they lit up my analysis spreadsheet green in every single category. When they announced the merger with Bwin Party I watched the share price as it dropped. This is the only time I actually timed my entry right, buying at 422p just before they climbed relentlessly to 687p following the merger, then moving onto the premium listing, then announcing a re-financing deal which will see them return to paying dividends in 2017. Over the next few months they will join the FTSE250 when all the tracker funds will be obliged to buy them, so I can only see the share price heading further upwards. My biggest regret is that I didn't move them into my ISA. It means I won't keep them forever, but am unlikely to sell below £10 a share. That would give me £3,520 (139%) profit, which I think would be a good outcome. The alternative would be to bed them into my ISA, but I'm nervous about what might happen in that period where the shares are in limbo. I think taking the profit would be a better path, but may change my mind.

JLP:Jubilee Platinum 4.2%

Currently down about 4% and losing £84.19

This is the only share that I've bought in each one of my SIPP, ISA and standard share accounts.

It's been remarkably frustrating as the price has been so volatile. Every time news comes out there's a surge, followed by a trickle back down to 3p. It's been in loss for most of the time I've had it, but I still believe it has massive potential.

There are three main interest areas. One is currently producing chrome from tailings. This cleans out the chrome making the remaining tailings suitable for platinum extraction. The current proposal is to ship these tailings off to another producer rather than build a platinum processing plant for a relatively short period before moving to the main site of interest. This main site is another tailings processing operation and is in development and due to come on-line next year. This is significantly larger than the first site and will make lots of money. The third area of interest is massive, but awaiting a signature on the mining licence. This has been dragging on for the whole year that I've owned these shares, and is getting very frustrating. When it comes, there will almost certainly be a major re-rating of the share price.

Meanwhile the price of platinum is soaring, but as Jubilee don't produce any yet, it's not made any difference.

The plan is to keep the ISA and SIPP shares for the long term and sell the ones in the main portfolio when they get to about 100% profit, which I'm sure they will - eventually.

LOOK:Lookers 3.9%

Currently down 40% and losing £822.19

If is wasn't for

AFG:Aquatic Food being worse, this would be my nemesis share. It was meant to be a safe FTSE250 company. I bought originally at 179p because I thought it was cheap, then topped up at 173p as it was even cheaper. Now it's trading at 108.5p - ouch!

My fair price based on my analysis spreadsheet is 254p.

I could understand a startup company with no revenue or a high risk Chinese company taking a nose dive before recovery, but not a solid, well respected FTSE250 company making good profits every year and paying a dividend.

If it wasn't already nearly 4% of my holding and if I wasn't so annoyed with it, I really should be topping up at this price.

In the meantime my capital is trapped and I'll just have to wait patiently for the market to see sense and for this to get to my target value

TRX:Tissue Regenix 3.5%

Currently down about 5% and losing £69.99

I bought a small amount of these for 15.405p a share which are 9% up and making £51 profit. I thought the share was so great that I bought three times as much in my SIPP at 18.67p which are down 9% and losing £121.

The concept is great - designing tissue that can be used in skin and muscle grafts and which doesn't need to be refrigerated for transport. It's being adopted all over the world and I'm convinced will see the company bought out by one of the pharma giants.

All I hope is that the share price is given a chance to grow before that happens.

Meanwhile if the opportunity arises, I'd love to get this up to 5% of the holding while the price is still so low. I think anything under 20p is a bargain.

SLP:Sylvania Platinum 3.3%

Currently down about 15% and losing £186.09

How the hell did I end up with 3.3% of my holding in this one?

My investment in this share has been a bit of a disaster, with the price dropping massively in both my standard share account and new trading account, but in profit by £16.84 in my ISA. Ironically, it's only the ISA where I ever intended keeping the shares long term.

I expected the same to happen to this share as happened with the gold mines. As the price of platinum went up relentlessly, surely the share price should too?

Nope!

What really annoys me is the total basket case

LMI:Lonmin which should have gone bust, has managed to climb from 75p to 225p over the last 6 months, whereas Sylvania which has a much lower cost production has gone from 7p to 7.5p. So much for the rising price of platinum!

I shall breathe deeply and wait patiently for the market to see the value of these shares, and just hope the price of platinum doesn't drop again in the meantime.

My ISA holding is for the very long term, my standard share account is for medium term - maybe 100% profit, and my trading holding is for the very short term - maybe 25% depending on how fast it goes up.

ALM:Allied Minds 3.1%

Currently down 6% and losing £98.97

I'll freely admit that the main reason I invested in this is because Neil Woodford has. I can see the massive potential should any one of the companies under this banner start generating serious revenue. At the moment none of them are, so it's a slow burner wait-and-see share. Perfect for my pension where it will sit happily for the next 18 years. No plans to add any more.

AFG:Aquatic Food 3%

My nemesis share, currently down 60% and making a loss of £940.32

I bought the shares because the company fundamentals seemed sound - in fact it seemed like a crazy bargain at 35p, with my analysis spreadsheet showing a fair price of 396p. The potential upside looks too good to be true.

Unfortunately that seems to be the attitude of the market - it is too good to be true. There have been too many companies based in China list on AIM, take the listing money, drive down the price of the share, then de-list taking all the shareholders money. The fear of this happening seems to be keeping people away from this share.

However, I believe it's genuine. It has supply contracts to USA as well as within China. The listing was done to raise funds for additional processing facilities, which seems perfectly reasonable. The slowdown in China has caused them to put the plans on hold, but that seems prudent.

I recently added more of these shares, more than doubling my holding just before the ex-dividend date. That will get me £45 dividend next week, which is about a 3% return

The top-up purchase brought the average price down from 35p to 23.96p. With the offer price currently 15p I should seriously consider buying more - if I believe this company is for real - and I do.

NTBR:Northern Bear 2.6%

Currently down 9% and losing £124.27

These were in profit a week ago! These were bought because of their very strong fundamentals. They have a very small market cap of £8.4 million, partly due to only having 19.2 million shares in issue compared to well over 100 million for most companies. They have acquired other companies and pay a dividend, and are the epitomy of a good, solid business.

I should really have them in my SIPP or ISA - at the moment they are in my standard share account, which isn't for really long term investments. This is one that I just want to tuck away and not look at, with the hope that they just keep growing, because with s few shares in issue, if anything happens that makes people want to invest, the price will absolutely rocket. If it does, I don't want tax constraints to force me to sell prematurely. I think I need to bed these in my ISA!

LGEN:Legal & General 2.4%

Currently up 7% and making £94.42

I had my eyes on these for a long time as a potential pension fund share, as they are secure and pay a 6.28% dividend.

As soon as I saw the Brexit crash, I decided this was the share I would buy in order to take advantage of the inevitable rebound.

I'll keep adding my monthly SIPP savings of £160 to this until the share price gets back to pre-Brexit levels of around 240p, which may not be long as they are currently at 213.5p. That should give me enough to keep as a long term holding.

TW.:Taylor Wimpey 2.3%

Currently down 26% and losing £311.55

Although there is much misery with this share, all thanks to Brexit, it's the one house builder I want to keep long term. I've had £62.28 dividend from this, which is 5.1% of the cost price. The dividend is guaranteed for the next 2 years even if there is a downturn in the housing market, as enough cash has been put aside already.

Great management, great dividend, and great prospects as there's no real sense of the housing demand decreasing. There may be higher costs to build them when we send all the workers back home and try and recruit local people who don't want to do the job, but the demand for housing is still strong.

If I wasn't so miserable about the state of my house builder shares, I would top up while these are so cheap, and I will transfer one of my existing house builders to here if I ever get to sell them.

UCG:United Carpets 2.2%

Currently down 12% and losing £150.63

Another small company with £8.6 million market cap. Their fundamentals are very strong and light up nearly all categories green. Just their tangible assets are a bit low for the price, but that's largely down to most stores being franchised rather than owned. My target price is 21p so I'm expecting them to double. I suspect the most likely outcome is that they'll be taken over, but ideally not until they've got past the Brexit blues and back into profit.

I'm planning to hold them long term, although if they go past PE ratio of 15 I'll probably sell. It's only 7 at the moment, so won't reach 15 until my target 21p. By then I'm expecting profits to have gone up so I can raise my target.

VEC:Vectura Group 2.2%

Currently down 9% and losing £101.83

I bought these for the long term, and the final tipping point was the merger with Skyepharma.

The fundamentals don't look great - in fact current fundamentals look dreadful. I'm completely relying on a massive amount of growth over the next couple of years.

I don't know if it will happen or not. If not then the shares are horribly over-priced and will plummet.

Actually, there's no way these should have qualified for me to buy them. I may have made a mistake...

DOTD:Dotdigital 2%

Currently down 8% and losing £81.70

This company has a PE ratio way higher than I would normally contemplate, at 29 when I go for below 15. I made an exception for these, as they had just been made platinum partners for the Magento e-marketing platform. I know Magento is huge, so the potential market this opens up is incredible.

It's been worrying watching the price go down from 51.89p to the low 40's, but it's back up to an offer price of 50p now, so gradually getting towards profitability.

I'm completely happy to hold these long term. No plans to add any more, and there's a small dividend to look forward to as well.

PAF:Pan African Resources 2%

Currently up 48% and making £503.34

This company has been very good to me. I initially owned it in my standard share account, making £360 (9.6%) profit plus £90 dividend. It slightly pains me to say that if I hadn't sold them I would be looking at a £2,936 (189%) profit.

I still mustn't grumble, as I bought back in at 14.935p and they are doing very well. This time they are in my ISA and will stay there for their 6% dividend. Gold will hopefully stay at these price levels for a while, which will keep them profitable and give me a target price. At the moment I don't have one, I'm simply not selling.

TLOU:Tlou Energy 2%

Currently up 3% and making £26.74

I bought this after hearing there was a gas company in Botswana that was about to hit the big time. I Googled Botswana Gas Shares and was happy to see this company listed on the LSE.

I did my research and came away really impressed with the management of the company. They've all been there and done it before, making loads of money in the process. As they say good management makes a good share, I bought a tentative amount at 4.1p. These immediately made loads of profit and i could see there was great momentum, so I nearly doubled my holding, buying the new shares at 7.2p. Guess what happened next - ooh yes, I had bought on a spike and they dropped back to 6p.

They are still making profit, and I'm still excited about the project, particularly as they have had approval for a power station five times the size of the one originally proposed. This is all in my ISA and I want to still be holding when they are generating power and selling both their gas and electricity. I don't plan to top up any more though.

TND:Tandem Group 2%

Currently down 50% and losing £545.03

This company has just 4.7 million shares in issue and a market cap of £5.05 million. Part of me wishes someone would just buy them and put me out of my misery.

I bought them on the basis that they were involved in franchised toys, particularly Star Wars which was due out soon and would surely mean loads of revenue.

What I hadn't counted on was just how badly their bicycle sales were doing, and it was that which caused a massive 30% drop in March. Things had started to recover, until Brexit which sent it collapsing to a 50% loss.

They do pay a dividend, so I will keep them - and lets face it, I don't want to lose £500 so there's no way I'm going to sell.

They won't be a long term investment, unless it takes long term for them to get into profit, as I'll sell straight away unless there's more positive news on sales.

CLLN:Carillion 1.9%

Currently down 4% and losing £42.81

This was a bit of a contrarian move. I'm not sure it was a good one, but let's see.

I bought this because it was the most shorted stock, with over 20% of its shares on loan for shorting.

OCDO:Ocado has now taken that crown, with only 18.4% of Carillion shares now on loan. I basically wanted to cock a snoop at the shorters, as I detest shorting and the damage it does to companies and investors. I wanted there to be some big news causing a mass panic of shorters closing their positions resulting in an exponential rise in the share price. I still hope for this, but am less convinced it will happen.

The reason I may have made a mistake is Carillion's colossal debt. I normally go for less than 3 times profits, but here it's 15 times profits. The glimmer of hope is that the majority isn't due for repayment until 2020, by which time I'm hoping the short closure will have happened, I'll have pocketed next year's massive dividend, and sold the shares. At the moment I'm not planning on these being a long term holding, despite them being in my SIPP. In fact, when they get back into profit I may just dump them and up my

TRX:Tissue Regenix or

CAML:Central Asia Metals holdings, because I like them much more than this.

RDT:RedT 1.9%

Currently down 10% and losing £98.90

I'm dead excited about this share, and should really be buying more. A Vanadium Redox battery the size of a container truck linked up to a wind farm can store all the excess electricity, then feed it back into the grid when the turbines are under capacity. The same goes for solar farms at night. This is exactly the technology the world needs to make renewable energy work.

There are other manufacturers inventing other types of battery, so this one needs to demonstrate it's the best for RedT to really fly. It's a risk, but it's an exciting risk with potentially massive rewards. Alternative power and electricity storage is the post-fossil fuel future, so now's the time to start investing in it. Gosh, I'm excited writing about this - maybe I should get some more!

RDW:Redrow 1.9%

Currently down 24% and losing £254.04

A house builder with very, very strong fundamentals. I managed to buy them just before house builders started to drop, and then Brexit hammered them good and proper.

They are in my standard share account so I don't think I'll keep them long term. What I might do is wait until they get into profit, which they will at some point, then move the proceeds to my ISA and use them to increase my holding in

TW.:Taylor Wimpey, as one house builder is enough for me.

SGRO:Segro 1.9%

Currently down 5% and losing £47.34

My only REIT, and I really like them and the concept of buying warehouses, particularly with the increase in on-line shopping.

Their fundamentals are mega, they pay a reasonable dividend, and I believe they have loads of scope for growth.

Although they were hammered by Brexit, they have recovered better than the house builders and I think will very soon be in profit as the offer price is only about 8p below the price I paid, and they often move that much in a day.

I used to have more of these, with some in my standard account. I sold those for a tiny £15.56 (2.4%) profit but intend holding the current ISA shares for the long term.

KIBO:Kibo Mining 1.8%

Currently up about 25% and making £293.48

When I bought these it was based on the companies fundamentals. Everything except cash flow was green. When I investigated further, I was intrigued by the plans for a coal to power project in Tanzania. Kibo own the coal mine and propose building a power station at the mouth of the mine. All the licenses and feasibility studies are being completed and the share price is starting to reflect the optimism that things will happen. There's also a joint venture gold mine that's being brought on-line given the increasing price of gold.

This share has been even more volatile than

JLP:Jubilee Platinum, and is one I may look at for my trading account. I've not wanted to try trading it, as I don't want to be out next time the spike stays in the upward trajectory. This is something I'm only willing to do with a specific trading account, so my investment shares are for the long term.

Having said that, about 40% are in my standard share account, so if there's an opportunity I may sell them and shift to the ISA and then buy back - if only I can pick the right time to do it!

HMI:Harvest Minerals 1.5%

Currently down 1% and losing £12.26

A fairly recent purchase. I already have two potash shares, but this one looked cheap for the potential profits to be made. Everyone needs fertiliser, so although this is in Brazil, it feels like a safe bet. It's not in my ISA so I don't intend to hold for very long, but with production on the near horizon I think this should be good for a potential 100% gain.

I do have to recognise that this was purchased with no basis of financial analysis and is pure speculation. It's the sort of thing I should restrict to my trading account if I'm going to do it again in the future.

MSLH:Marshalls 1.4%

Currently down 25% and losing £183.03

This share was meant to be another safe FTSE250 share, but is also struggling thanks to the same sentiment that's bringing down the house builders. It has good fundamentals, although does miss the mark on a few things, but my target price is 375p compared the the current 273.8p. The problem is I bought these for 351p before I had my analysis spreadsheet. 24p wouldn't have been enough of a potential rise for me to buy them, so these should never have made it to my portfolio.

I will hold to 375p, which may take some time. It's possible that when they post more results, my target price will lift before I sell. These are in the standard share account so are not a long term hold.

AFPO:African Potash 1.3%

Currently down 88% and losing £622.42

I bought these at 1.876p on the great promise of a wonderful story. As the price went up I bought more at 3.2p, riding the wave of momentum. The selling factor was a deal with COMESA to supply fertiliser across Africa. The trading operation would generate income to fund the potash mine being developed in DRC. Eventually they would supply their own potash and the profits would come rolling in.

Tragically the first deal went wrong. Thousands of tons of fertiliser stuck in a Tanzanian port when the buyers pulled out of the deal, citing drought in Zimbabwe as the reason for not needing the fertiliser. Needless to say the share price tanked to 0.35p.

I had pretty much given up hope, expecting to hear the company had gone into administration. However, the last few weeks have offered a glimmer of hope. New deals have been struck and fertiliser is being supplied. We just don't know whether it's enough to keep the company solvent, let alone provide the income to start up the potash mine.

If it is enough to enable the company to survive, then an offer price of 0.4p is a mega bargain. I think it's too high a risk for me though, so I'll hold out with my 27,860 shares and hope for recovery.

BDEV:Barratt Development 1.3%

Currently down 37% and losing £248.45

One of my first shares. I bought it for the strong company fundamentals, good dividend and unbroken climbing chart over the last few years. It was meant to be a good, safe FTSE100 share.

That was before threats of increasing interest rates, extra stamp duty on buy-to-let, and the nail in the coffin Brexit.

I'm still confident this will recover, and it does pay a good dividend. I have £26.30 dividend so far. However, it could take years to get back into profit. I am happy to hold though.

Once it does get back into profit, I will sell. I feel over exposed to house builders at the moment, so will aim to consolidate in

TW.:Taylor Wimpey which has put aside enough cash to guarantee big dividends for the next 2 years even if there is a downturn.

In the meantime I just have to wait for this one to get back into profit.

ARL:Atlantis Resources 1.2%

Currently down 35% and losing £232.96

I managed to buy this right at the top of a spike, excited by news they had connected their underwater turbine site to the national grid with a very long cable and were about to install the first turbine.

Since then it's all gone quiet and the share price has dropped relentlessly. I must learn the right time to buy a share!

This is in my SIPP so it's a long burner. I think it's a great concept to have massive under-sea tidal turbines. So much better than tidal barrages for the environment. There's already work in Indonesia where this company could revolutionise electricity supply to the hundreds of islands that make up the country. I'm happy that if the share price could get to where I bought based on promise, it can get back there based on fact when the power is being generated. No plans to top these up though.

WRES:W Resources 1.2%

Currently down 50% and losing £281.98

This share is a good example of how it's a bad idea to buy something just because it's so cheap you get loads. I bought 98,735 shares - wow!

They are however utterly worthless and have halved in value.

There is a modicum of hope, as blasting has commenced in the mine so we may actually be able to produce something soon.

This was one of my early purchases - I don't think I would buy them if I stumbled across them now, and if they ever get remotely close to my target of 1p I'll be very happy, and sell them quick.

WRL:Wentworth Resources 1.2%

Currently down 25% and losing £164.25

These were one of my earliest shares. I can't even remember how I found them.

I was excited that they had just started production of gas and would immediately start generating revenue.

Things have been distinctly quiet since then, and the share price has dwindled to a 25% loss. However, some analysts believe it could go over 100p a share. I'm not sure on what timescale, but for now I'm happy to sit and wait, but I won't be adding any more.

IKA:Ilika 1.1%

Currently down 15% and losing £87.60

This was purchased as a speculative buy based on my current obsession with batteries.

They have developed a tiny lithium battery that contains no liquid and can operate at extreme temperatures.

It can be trickle charged quickly by solar cells, so is ideal for sensors used in the Internet of Things.

They have close ties to

ARM:ARM Holdings and are planning to develop a similar model where they licence the battery technology but do not actually manufacture the batteries.

It's a shit or bust share really. Either the battery will be adopted and they will soar, or there will be better alternatives and it will go bust.

At the moment the market seems to be thinking the latter, as the shares have dropped from my purchase price of 55.6p to 50p.

These are a long term hold in the ISA, and I suspect if they do take off, it's most likely the company will be bought out by one of the big players - maybe even by ARM themselves.

EMH:European Metals 1%

Currently down 19% and losing £95.63

I bought these once before and they went from 9.75p to 13.02p and made me £168 profit, so decided they had further to go and bought again. Unfortunately this time I timed my purchase really badly, and they were right at the top of a spike. They've since dropped right back from 23p to 20p so are losing money.

I have to admit I bought them for short term gain rather than long term investment, although I do believe they are an excellent long term prospect. However, these are the main reason I set up a separate trading account, so I don't make the same mistake again. Oh hold on - I did make the same mistake again and bought on a spike in that account too!!

Meanwhile I'm confident these will do well, but if they get into profit before early September I'll certainly sell them to pay for my holiday.

IOG:Independent Oil & Gas 1%

Currently up 47% and making £256.48

I found this when going through my A-Z of shares and it lit up everything green except cash flow. Given the PE ratio of 2 I figured there was a lot of potential, with a fair price of 83p. I bought at 15.325p and it's now at 23.375p and they haven't even announced the results of the drilling yet.

There's still a risk that oil prices could fall further, but the fundamentals of this company look strong enough to withstand it. If they start paying dividends I'll be keeping for the long term, else I'll review when they get to 83p. I may also top up and double my holding if I get free cash before they go up too much further.

JLG:John Laing Group 0.9%

Currently down 1% and losing £6.94

I had these as my auto-purchase SIPP shares for the first 3 months, as I've had shares in this company before and really like it. Last time I sold them for £42.48 (4.8%) profit because I desperately wanted to get something else. This time I'll hold long term, and once

LGEN:Legal & General gets back to pre-Brexit levels, I'll put my monthly saving back on here until I build up £1,000.

One of the things I like most about this company is that the directors are bought up to the hilt in shares - so they have huge incentive to do well. They also have very strong fundamentals, with cash flow the only weakness. The dividend is ok too, at 3.2%.

CRL:Creightons 0.8%

Currently up 16% and making £64.12

I bought a small amount of these soon after developing my analysis spreadsheet, as their fundamentals lit everything up green. They have a tiny market cap, but have made acquisitions to expand their product range, and are making good profits.

Their spread is 9% which put me off getting more, but as a value investment they are very strong, so I should really have this on my list for consolidation as I sell off some of the marginal shares.

Their tiny size also makes them ripe for takeover, although I'd rather they just continued to grow and become the next Unilever!

RDT:Rosslyn Data 0.7%

Currently down 54% and losing £194.30

These were a bit of a punt when I was starting out. I was persuaded by their big-name clients and couldn't understand why the share price kept dropping. They only listed recently and so have not made a profit yet. I can't really tell if they are likely to either.

Buying them was a mistake, and I wouldn't go near them now, but I don't intend selling, especially as it would liberate such a small amount.

The one ray of hope is that there was a rumour Microsoft may want to buy them out. Probably not true as nothing came of it, other than a brief upwards spike of the share price - tragically not enough to take my holding into profit. I'll just wait patiently and hope they don't go bust.

SXX:Sirrius Minerals 0.3%

Currently up 51% and making £94.85

One of my first purchases and bought after watching an article on Countryfile

It looked really risky so I bought just 1,000 shares at 17.32p. They spent most of the year around 12p as nobody really thought the project would get going. However, as confidence has slowly built, people are taking notice and the price is moving steadily upwards. I now regret not having believed it myself at 12p, because I'm now concerned the current 29.5p is a spike, and I'm fed up of buying on a spike!

If they drop back down to around 23p I may consider upping my investment from this rather tiny holding. Having said that, it's making more profit than most of my shares!

BLUR:Blur Group 0.2%

Currently down 86% and losing £94.35

My biggest disaster of a share, but thanks to only paying out £109.40 in the first place, protected from too much loss.

I bought them when I didn't know what on earth I was doing, and looked at the 52-week low report to find a share price I was sure could only go up. The big mistake was failing to examine why the share price was so low. Clearly the company is in trouble, with massive cash burn and not enough revenue to cover it. They have tried to re-invent themselves and focus on repeat income from enterprise customers, but at the moment they don't appear to have anywhere near enough to stay in business much longer.

I hold them as a reminder of what not to do.

TRK:Torotrak 0.2%

Currently down 57% and losing £60.58

Another disastrous purchase when I didn't know what I was doing and picked a share because it was the lowest it had ever been.

If I'd just read the bulletin boards I would have heard all the disgruntled investors moaning about poor management, great ideas failing to be marketed, and still no sign of a commercially successful application for their KERS system.

There was hope when the VW scandal broke - would this force diesel cars to adopt greener technology and get the system into a car. Nope!

Somehow they manage to stay in business, and some day they may get the system in a car, but in the meantime I'm really glad one of the other symptoms of not knowing what I was doing was I only invested £106

PUR:Pure Wafer 0%

Currently suspended awaiting liquidation.

This company de-listed after their UK factory burnt down and they re-located to their USA factory.

The insurance money for the fire and sale price was paid back to shareholders.

At the moment this is resulting in a £9.35 loss, but the shares are held in a suspense account awaiting the final liquidation, at which time an estimated £45 will be paid to shareholders.

In the meantime I keep them on my portfolio listing with a £0 cost and £45 profit. In theory this should all be wrapped up in September, so not too much longer to wait.

Phew - that's me completely knackered. Some really good insight has developed while writing that. Just ordering them by percentage of the portfolio was a revealing exercise. I know exactly which shares I want to top up and which I want to get rid of, so now we just sit back and wait for things to happen...